9.2%

10 year return¹

Focused Growth fund performance

8.3%

10 year return¹

Industry average for Aggressive funds

Morningstar is an independent investment research firm that compiles, analyses and ranks KiwiSaver funds.

Exceptional and awarded service

We’re not a faceless provider, quite the opposite. We talk directly with members coming on board to make sure they’re well informed and their KiwiSaver plan is right for their goals.

Consumer NZ People's Choice

Customer satisfaction award

Canstar Award

Most Satisfied Customers - KiwiSaver

Trusted Brand Award

Reader’s Digest Trusted Brand Award for KiwiSaver

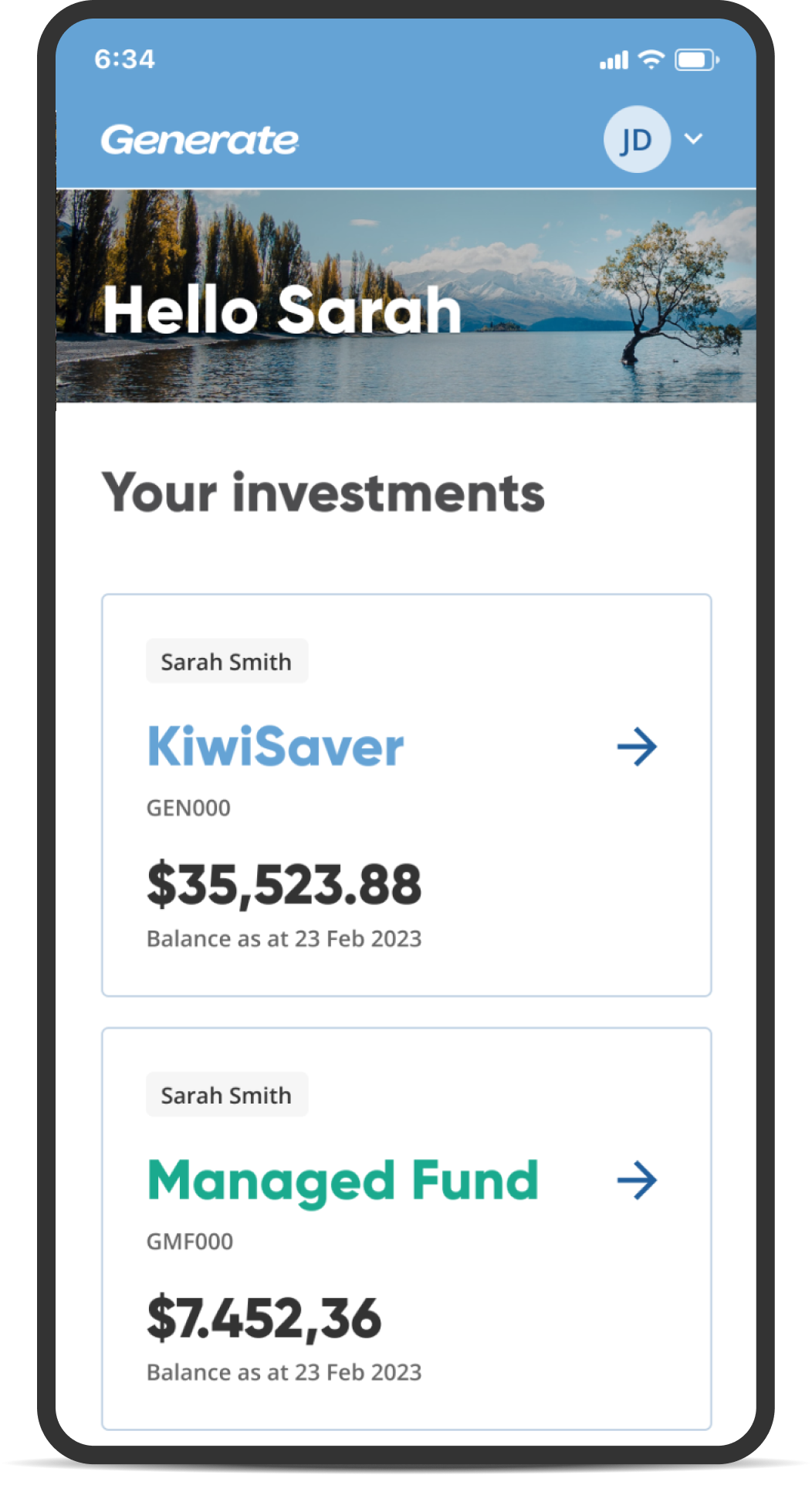

Your fund performance at your finger tips with the Generate App

Disclaimers